You can assume that both the sales and the purchases are on credit and that you are using the gross profit to record discounts. Regularly assessing stock levels and maintaining accurate records can be facilitated by a periodic inventory system. A periodic inventory system is a simple and economical way to keep track of inventory levels and costs. It requires less effort to set up and maintain than other inventory systems, making it an attractive option for many businesses.

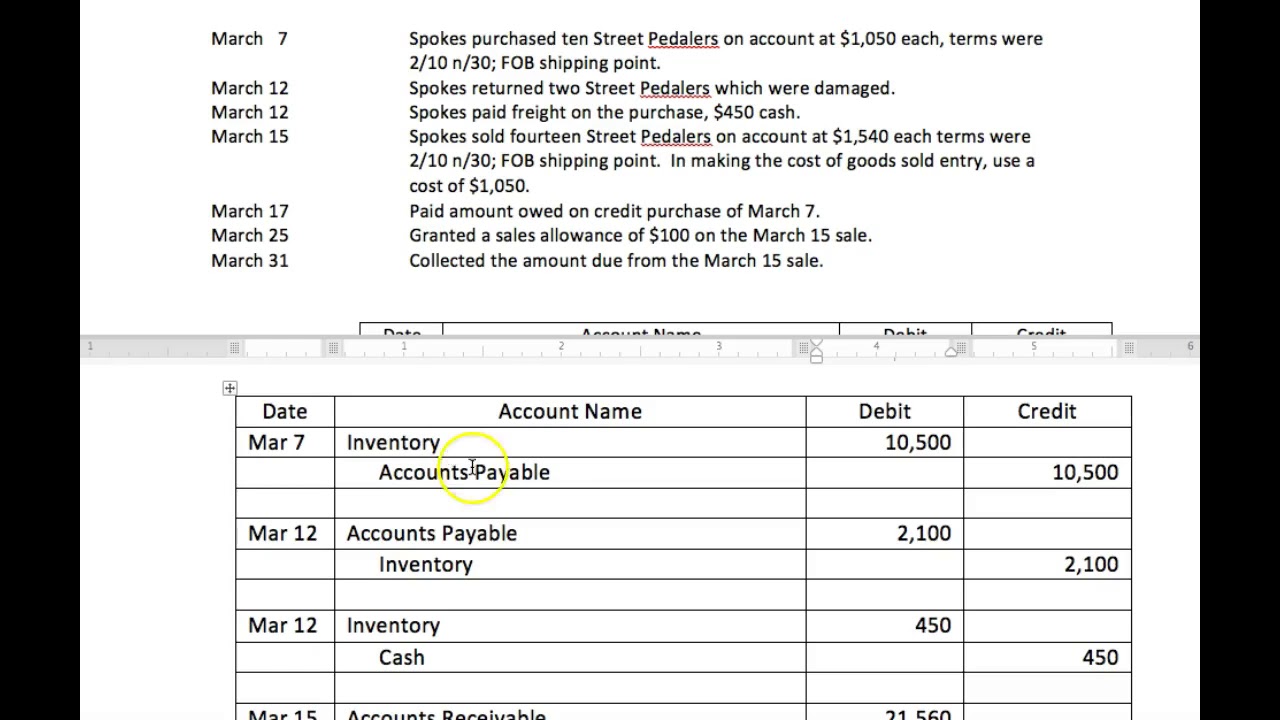

Perpetual Journal Entries

- At the end of the year, or at the end of any other timing interval businesses choose, a physical inventory count is done, to recognize the amount of remaining inventory.

- Since there is no constant monitoring, it may be more difficult to make in-the-moment business decisions about inventory needs.

- A periodic inventory system can help businesses stay organized with minimal effort and cost.

- It’s a straightforward way to manage inventory, but it also means stock numbers are only accurate right after the count is completed.

- To maintain consistency, we’ll use the same example from FIFO and LIFO above to the calculate weighted average.

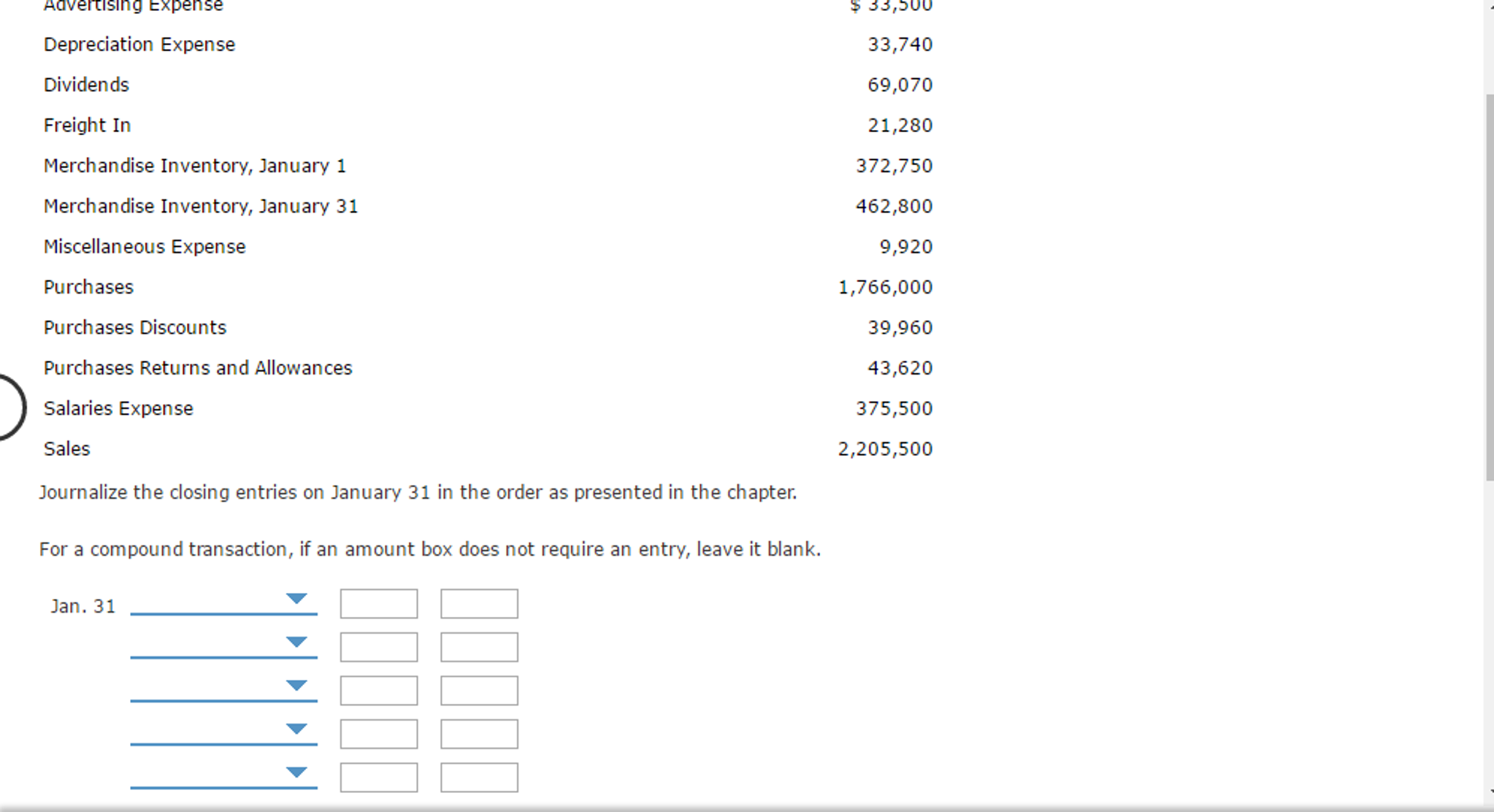

Under the periodic inventory method, cost of goods sold is calculated at the end of the period only and recorded in one entry. In the periodic inventory system, GAAP standards require a business to maintain a ledger where it can record 10 characteristics of financial statements its types features and functions the cost of inventory during the course of an accounting period in a “purchases account.” One of the most straightforward accounting procedures that enable a corporation to track its entire inventory is periodic inventory systems.

Examples of Periodic Transaction Journal Entries

Additionally, since the stock is only updated occasionally, more resources are available for other corporate operations. This journal shows your company’s debits and credits in a simple column form, organised by date. A perpetual system is superior to a periodic system in many ways, especially for companies that are considering their longevity. A perpetual system can scale, so whether you have five products (today) or 200 products (tomorrow), a perpetual system can effectively manage inventory control. Periodic inventory is an accounting stock valuation practice that’s performed at specified intervals.

Financial and Managerial Accounting

On the other hand, in a periodic inventory system, inventory reports and the cost of goods sold aren’t kept daily, but periodically, usually at the end of the year. A periodic inventory system also requires manual data entry and physical inventory counting. A periodic Inventory System is defined as an inventory valuation method in which inventories are physically counted at the end of a specific period to determine the cost of goods sold. That means ending inventory balance is updated only at the end of the period instead of a perpetual inventory system where inventories are counted frequently. Conducting regular physical counts of stocks is an essential part of verifying and maintaining accurate inventory records. Companies need to take into account the stock levels of their products in order to plan for future orders and to ensure that their records are always up-to-date.

Settlement of Accounts Payable

A basic count during the day or week is often enough for a small business to get an adequate handle on their inventory. This means there is no need for expensive or complicated equipment, just essential information collection tools – pen and paper. With the periodic inventory method, the ending inventory from your previous physical count becomes the beginning inventory for the next period. For instance, if a retail company doesn’t have the right amount of inventory to meet customer demands, it will lose sales. Production might have to stop for a few hours or days, and the company will lose money because it still has to pay its employees, rent, and more.

Everything to Run Your Business

Due to the development of tools like barcode scanning and inventory management software over the years, the perpetual inventory system has grown in popularity. However, most small business owners appear to have a soft place for the periodic inventory system. It’s crucial to comprehend exactly what a perpetual inventory system is before we discuss its distinctions. Small firms that handle a modest number of transactions or enterprises with a small inventory are the primary users of the periodic inventory technique. These businesses typically choose a periodic inventory system since it is easier to operate and more cost-effective because their sales and costs are simple to control.

The physical counting approach to the inventory management system is through periodic inventory system techniques. It is done regularly to determine inventory data that affect the cost of goods sold. Periodic inventory control is a difficult task that requires time and effort. As a result, small enterprises with little need for inventory typically use the periodic inventory approach.

For this reason, buyers record purchase returns and allowances in a separate Purchase Returns and Allowances account. Under the periodic inventory system, when company makes sales, they only record the revenue and accounts receivable/cash. The journal entry is debiting accounts receivable or cash and credit sales revenue. A purchase return or allowance under perpetual inventory systems updates Merchandise Inventory for any decreased cost. Under periodic inventory systems, a temporary account, Purchase Returns and Allowances, is updated.

Even though periodic inventory is simple to execute, there are several significant downsides regarding the quantity of detail you receive and how frequently your data is updated. Most business owners and managers require up-to-date information daily to make wise business decisions. With each sale or shipment, most large enterprises immediately update their inventory. When you buy anything in a physical shop or online, the merchant has complete knowledge of what was purchased and when allowing them to plan for restocking. A sales allowance and sales discount follow the same recording formats for either perpetual or periodic inventory systems. A perpetual inventory system automatically updates and records the inventory account every time a sale, or purchase of inventory, occurs.

This purchase account can be a temporary account to hold all the inventory purchases for a given accounting period. Setting up a periodic inventory system is an essential part of maintaining accurate stock records. It involves establishing a system that routinely checks the stock levels of inventory and keeps track of any discrepancies between the actual stock records and the recorded inventory. Physical inventory counts also help to identify any discrepancies between the physical and the recorded stock levels. This helps in ensuring that the stock levels are accurate and that any discrepancies can be rectified.

While the periodic method is acceptable for companies that have minimal inventory items or small businesses, those companies that plan to scale will need to implement a perpetual inventory system. Regardless of the type of inventory control process you choose, decision makers need the right tools in place so they can manage their inventory effectively. NetSuite offers a suite of native tools for tracking inventory in multiple locations, determining reorder points and managing safety stock and cycle counts. Find the right balance between demand and supply across your entire organisation with the demand planning and distribution requirements planning features. This is in contrast to the perpetual inventory method, another inventory management system that has become popular due to advances in technology.